Global commercial insurance prices decreased by an average of 4% in the second quarter of 2025, continuing the downward trend seen in the first quarter, which recorded a 3% drop, according to Marsh’s latest Global Insurance Market Index. Marsh is the insurance brokerage arm of Marsh McLennan.

However, this general softening of the market did not apply to casualty insurance. In fact, global casualty rates rose by 4% for the third consecutive quarter, with the U.S. market driving much of the increase due to continued escalation in claim frequency and severity — particularly those involving large jury awards, often referred to as “nuclear verdicts” (defined as awards exceeding $10 million).

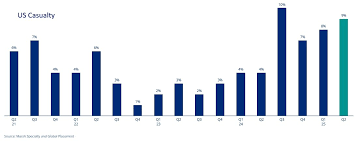

U.S. casualty premiums surged by 9% in Q2 2025, following increases of 8% in Q1 and 7% in Q4 2024. According to Marsh, this rise is largely due to ongoing claims inflation and the financial impact of high-profile legal settlements.

“Intensifying competition among insurers with aggressive growth goals is leading to reduced prices and broader coverage offerings. However, the continued rise in U.S. casualty rates remains a concern for clients,” said John Donnelly, President of Global Placement at Marsh.

Q2 2025 marks the fourth consecutive quarter of declining composite insurance prices globally, continuing a broader softening trend that began in Q1 2021 after seven years of rate increases. Marsh attributes this trend primarily to increased competition among insurers, which has expanded market capacity and driven more competitive pricing and coverage.

“In this quarter, clients generally benefited from both price reductions and enhanced policy terms. Major carriers pursued ambitious growth strategies, supported by favorable reinsurance pricing, which contributed to a highly competitive marketplace,” the report noted.

Regional Rate Trends

Composite insurance rates fell year-over-year across every global region in Q2 — except the U.S., where rates remained unchanged.

-

Pacific saw the steepest drop at 11%, followed by the UK with a 6% decrease.

-

Asia, Latin America and the Caribbean (LAC), and India, Middle East & Africa (IMEA) all saw declines of around 5%.

-

Canada and Europe experienced 4% reductions.

Global Property and Specialty Lines

Property insurance rates dropped by 7% globally in Q2, following a 6% decline in Q1. Regionally, the U.S. and Pacific markets led the decreases with reductions of 9% and 13%, respectively. Other regions saw declines ranging between 4% and 7%.

Financial and professional liability coverage saw global rates fall 4% in Q2, a slight moderation compared to a 6% drop in Q1. All regions posted decreases except the U.S., where rates held steady.

Cyber insurance pricing declined globally by 7%. Notable regional drops included 17% in Latin America and 15% in Europe. In the U.S., cyber premiums fell 3%, marking the ninth consecutive quarter of price reductions.

U.S. Casualty Market in Focus

In the U.S., casualty insurance rates jumped 9% in Q2. Excluding workers’ compensation, the increase would have been 12%.

Marsh highlighted several factors influencing this segment:

-

Auto liability premiums continued to rise, impacted by growing claim severity, higher repair costs, and “nuclear” verdicts.

-

General liability (GL) pricing was mostly flat, though certain industries like real estate, hospitality, and public entities faced premium increases due to higher loss activity.

-

Some insurers introduced alternative program structures — such as higher retentions or corridor deductibles — particularly for large clients.

-

Coverage exclusions became more common in GL policies, especially for risks tied to PFAS, biometrics, cyber exposures, and issues such as sexual abuse and human trafficking.

U.S. Umbrella and Excess Liability Developments

In the umbrella and excess liability market, rate increases remained significant:

-

Risk-adjusted umbrella rates rose 18%, up from 16% in Q1.

-

Standard excess liability rates increased by 14%, continuing the same pace as the previous quarter.

-

Carriers often reduced their offered limits, with some capping capacity at $10 million per risk due to the ongoing legal environment.

-

Programs with favorable loss histories saw lead umbrella premiums rise between 12% and 15%, while accounts with negative claims experience faced hikes of over 30%.

The exit of four London-based capacity providers in 2024 further tightened the market. Some excess carriers also raised minimum premiums to $10,000 per $1 million in coverage, leading to increased pricing for umbrella coverage.

Marsh noted that insurers are shifting away from single-tower structures in favor of supported umbrella layers due to heightened concern over loss frequency. Additionally, the growing influence of third-party litigation funding has led underwriters to prioritize renewal pricing that reflects estimated annual cost inflation in the 12% to 15% range.

In auto liability, insurers have responded to rising claim frequency and severity by raising attachment points, especially for large fleets in high-risk U.S. states. Carriers also sought to impose limitations on coverage for emerging risks such as PFAS contamination and human trafficking.

Note: All percentage figures refer to average rate changes unless otherwise noted. For clarity, Marsh has rounded all data points on rate movement to the nearest whole number.